Spending and Budgeting May 28, 2026

The Pulse

June 3, 2026·0 comments·Money

Executive Summary

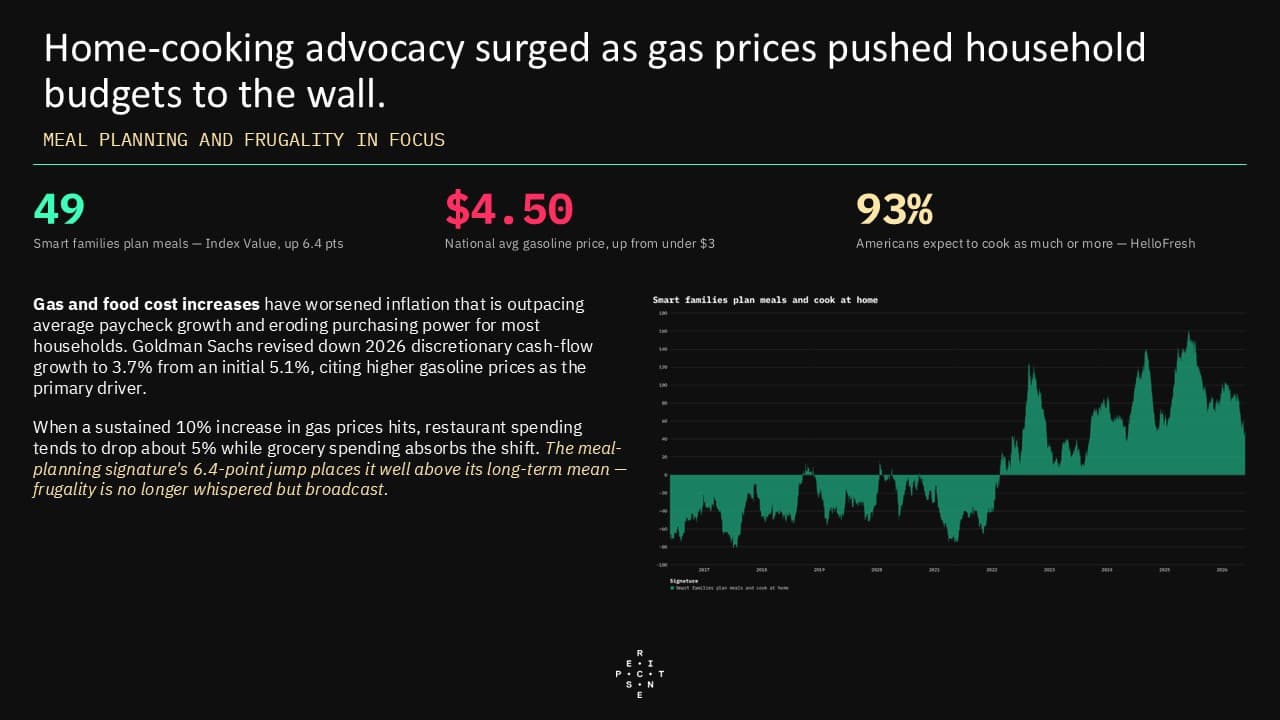

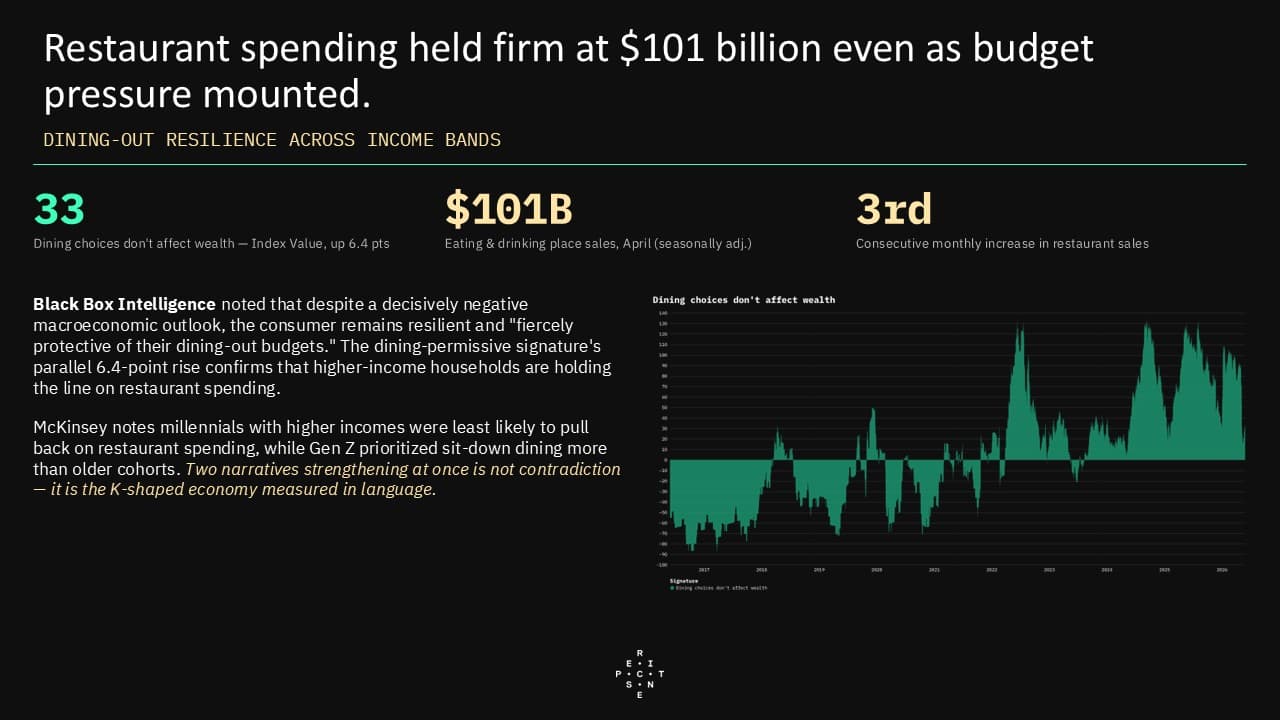

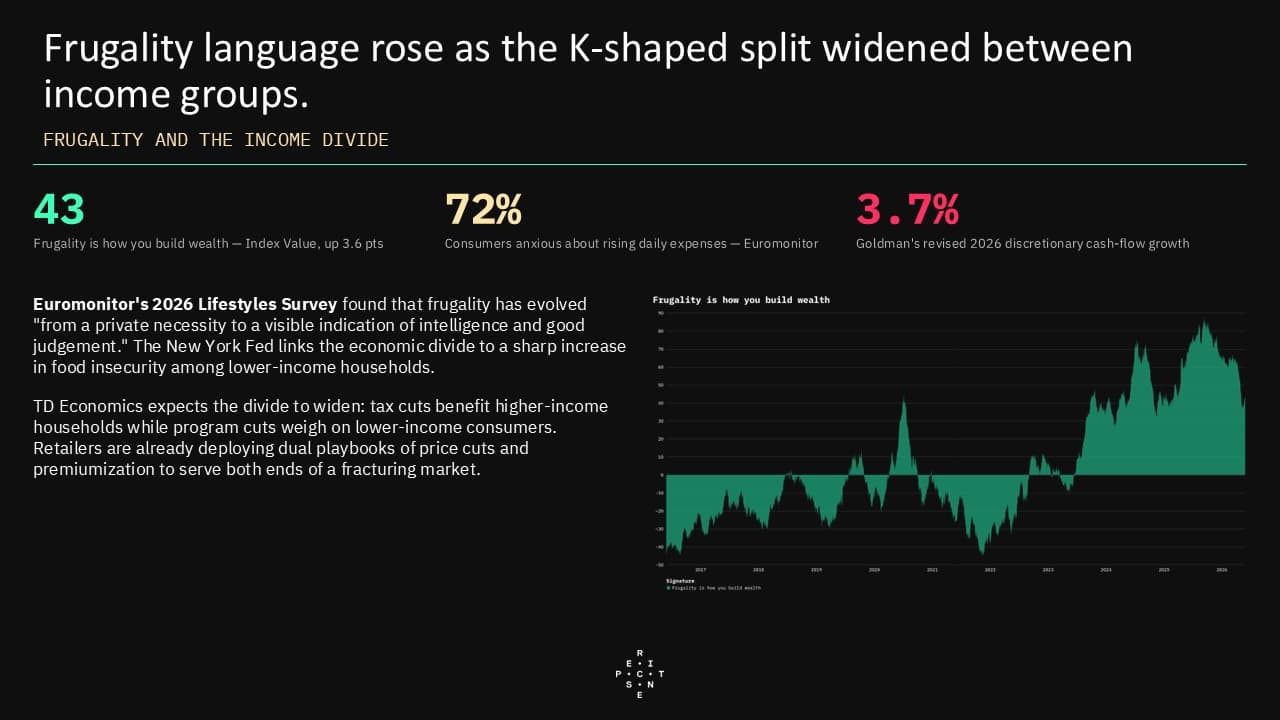

- Rising gasoline prices from the Iran conflict are fracturing household spending discourse along income lines rather than producing a single dominant narrative. Perscient's semantic signatures tracking both home-cooking advocacy and dining-permissive language strengthened in tandem, reflecting a K-shaped consumer economy in which lower-income households face growing food insecurity and turn to frugality while higher-income consumers remain fiercely protective of restaurant budgets. This dual strengthening — rather than one narrative crowding out the other — mirrors the retail industry's adoption of simultaneous price-cut and premiumization strategies and suggests that the food-spending media environment will continue to support both grocery-and-meal-kit operators and select restaurant chains, depending on which income segment they serve.

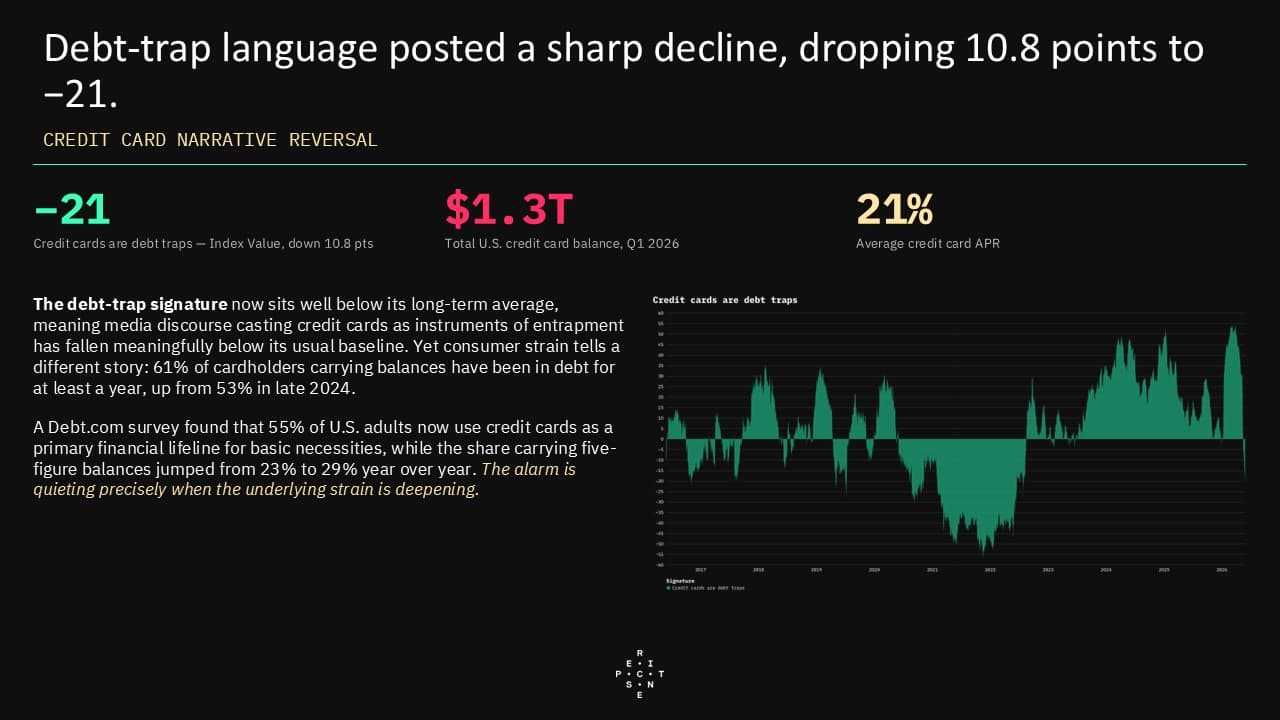

- Media warnings about credit card debt traps have receded sharply — posting the largest single-signature decline in the dataset — even though consumer financial strain continues to build beneath the surface. Credit card balances remain above $1.3 trillion, a growing share of cardholders report using credit for essential expenses like groceries and utilities, and revolving credit is expanding at one of its fastest rates since 2022. The quieting of alarmist credit narratives, combined with the persistent gas-price drag on household budgets documented in the food-spending section, suggests that media headwinds for consumer credit issuers are muted in the near term but could intensify if delinquency trends deteriorate later in the year.

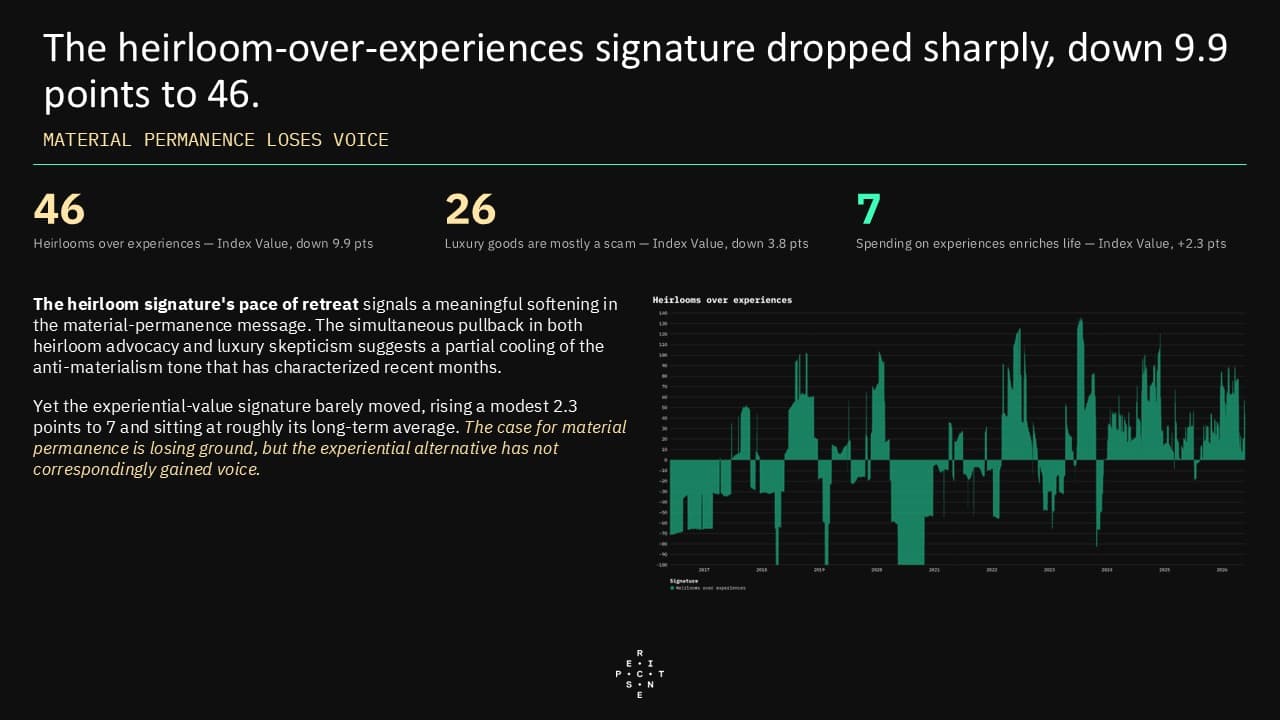

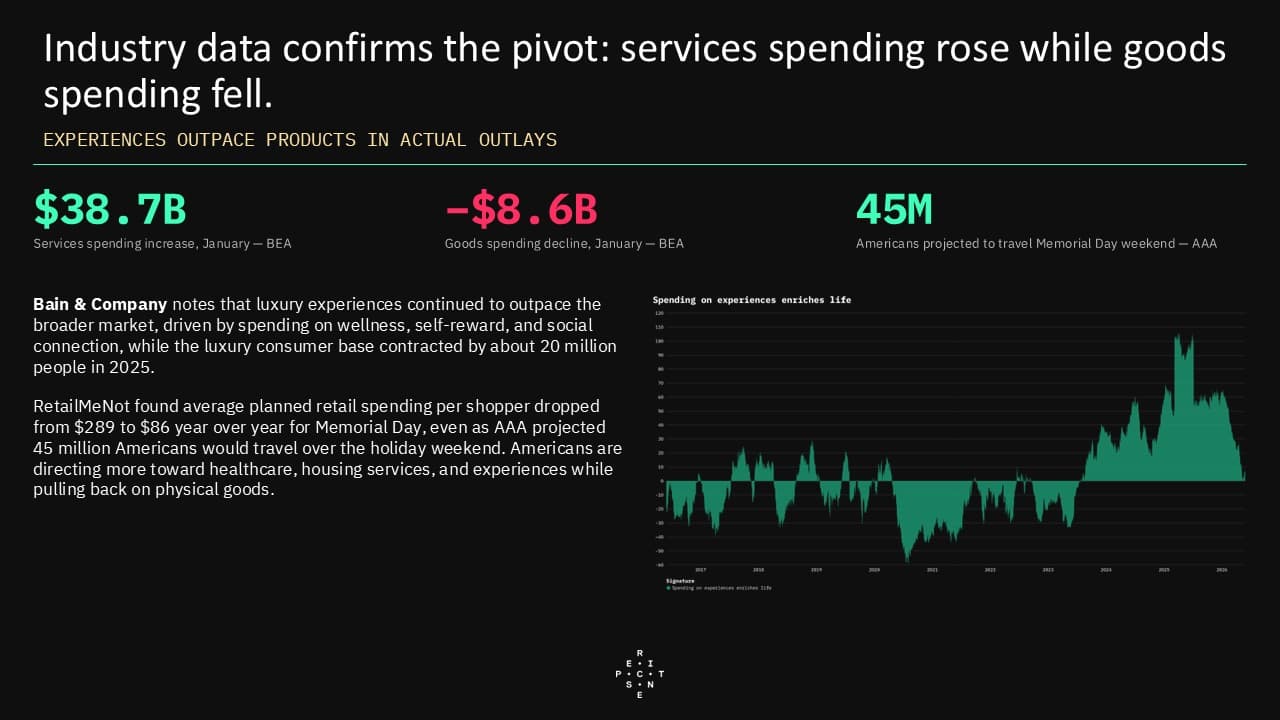

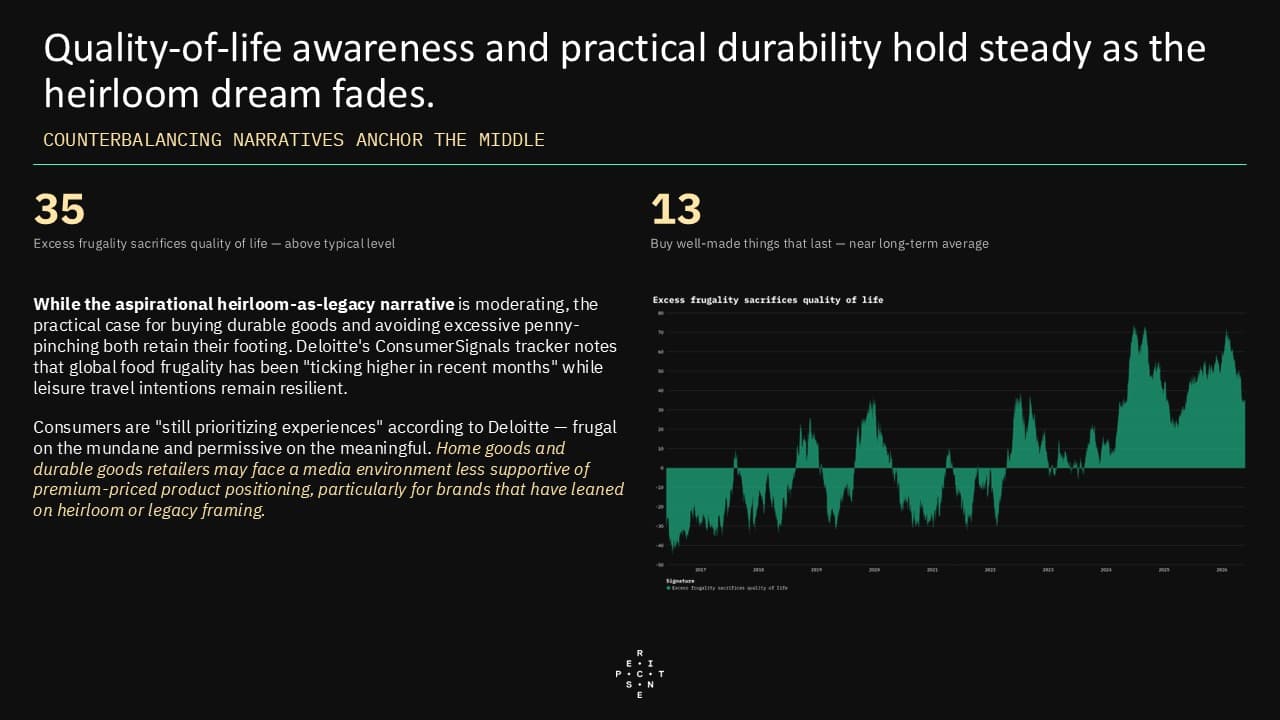

- The case for material permanence is losing voice in financial media while experiential spending language holds steady, reinforcing a structural consumer shift from goods toward services. Perscient's semantic signature tracking heirloom-over-experiences language posted one of the largest declines in the dataset, and luxury skepticism also softened, yet the experiential-value signature remained near its baseline. Industry data confirms the pattern: services spending continues to rise while goods spending contracts, and record holiday travel coexists with sharply lower planned retail purchases per shopper. Home goods and durable goods retailers may face a media environment that is less supportive of premium-priced product positioning, particularly for brands that have leaned on heirloom or legacy framing.

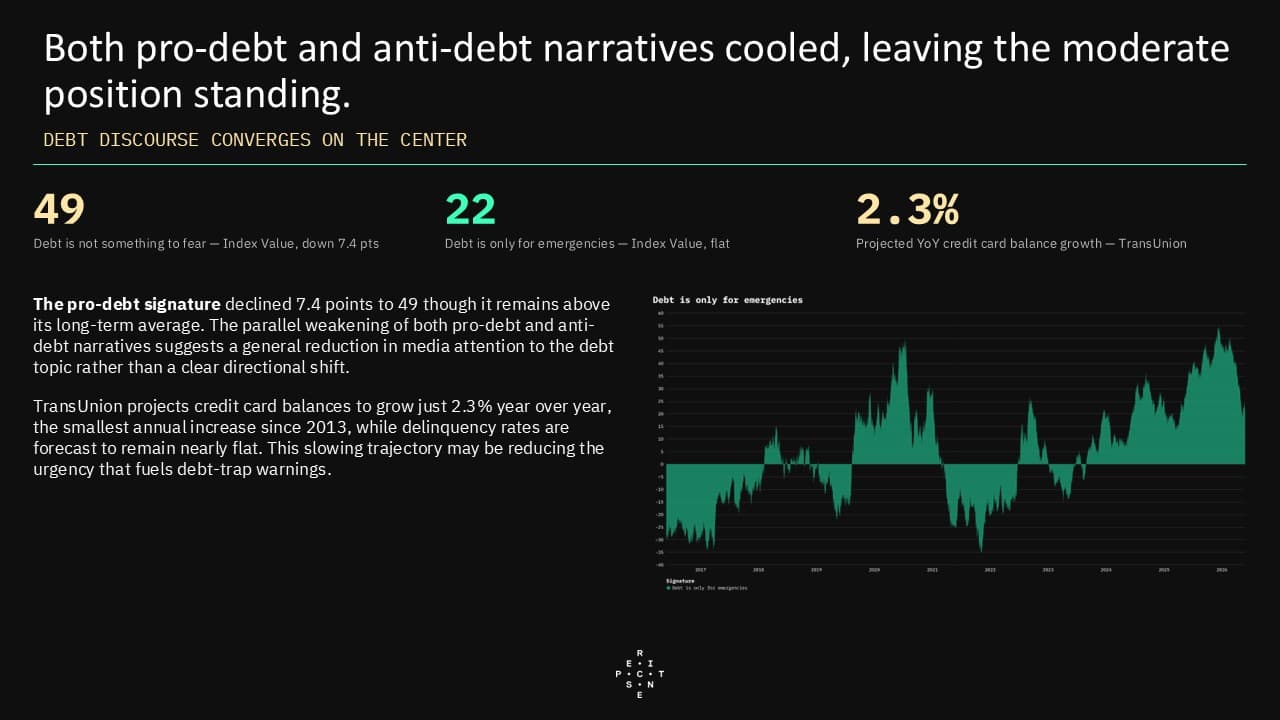

- Across all three spending domains — food, credit, and discretionary purchases — the unifying theme is that financial media is converging on a message of selective discipline rather than wholesale austerity. Frugality-focused language strengthened, but the narrative that extreme frugality harms quality of life held above its typical level, and both the pro-debt and anti-debt ends of the spectrum cooled while the moderate, emergency-only position held firm. Consumers appear to be cutting on the mundane and protecting outlays on experiences and occasions they consider meaningful — a pattern that favors hospitality, travel, and live entertainment sectors while pressuring undifferentiated goods retailers caught in the middle of the K.

Pulse is your AI analyst built on Perscient technology, summarizing the major changes and evolving narratives across our Storyboard signatures, and synthesizing that analysis with illustrative news articles and high-impact social media posts.

Pulse

Money